Multi-agent systems for financial trading. Sounds like a Wall Street quant fund's secret weapon — until you realize this project is open source, 73K stars, and anyone can clone and run it.

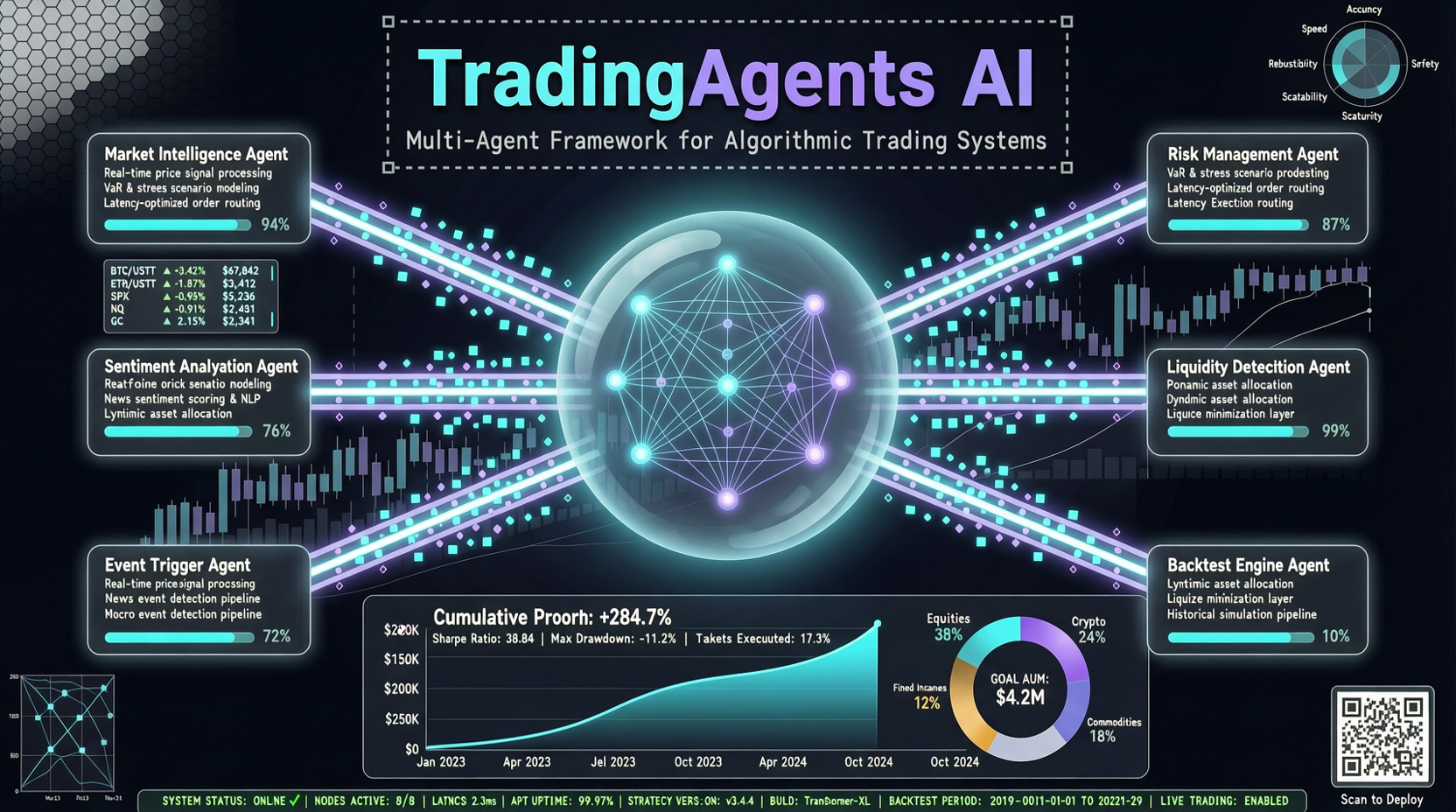

TradingAgents' architecture isn't complex: multiple LLM agents play different roles — researcher analyzes market data, trader formulates strategies, risk officer reviews risks, and finally a decision agent synthesizes all opinions to recommend actions. Not a single model making buy/sell calls on a whim, but a mini research team collaborating.

What it actually does

This project comes from TauricResearch and has been very active recently — a Grok 4.20 integration commit was pushed just 17 minutes ago. The supported model list is ridiculously long: Claude Opus 4.7, Grok 4.20, MiniMax, DeepSeek, Qwen, GLM — covering almost all major options.

But don't let the star count blind you. 73,315 stars, 14,284 forks, 221 open issues. Behind those numbers are two possibilities: either lots of people are actually using it, or lots of people cloned it, looked around, and closed the tab.

Check the commit history: only 164 total commits. For a 73K star project, that density is low. However, recent commit frequency is accelerating — two updates in the past few hours, suggesting the team is actively developing.

Multi-agent trading vs single-model trading

TradingAgents' core selling point is "multi-agent collaboration." How does this differ from asking Claude or GPT "what should I buy today"?

The difference is role division. A single model doing trading simultaneously takes on research, analysis, decision-making, and risk control roles, which can lead to overconfidence in one dimension. Multi-agent assigns different models (or different prompts of the same model) to specific roles, theoretically reducing systemic bias.

But "theoretically" and "in practice" are separated by a river.

Honestly: don't test this with real money

This isn't just my opinion. TradingAgents' README includes a disclaimer, and the issue section has discussions about the gap between backtesting and live trading. Financial market noise far outweighs signal, and LLM training data contains too much hindsight explanation — they're good at writing "why the market dropped yesterday" analysis reports, not predicting "what happens tomorrow."

If you use this framework for research, learning, or demos, fine. If you plan to connect it to your brokerage account for automated trading — run it on a paper trading account for three months first.

The real value of this project

The most valuable part of TradingAgents isn't "can it make money," but the multi-agent collaboration architecture it demonstrates. Research agent gathers data, analysis agent extracts signals, trading agent formulates strategy, risk agent evaluates risk — this pattern can migrate to many scenarios: supply chain decisions, medical diagnostic assistance, legal case analysis.

Financial trading is just a demo scenario.

Who should care

- Quant developers: Want to research multi-agent architecture in financial scenarios — worth looking at

- AI engineers: Want to understand practical multi-agent collaboration implementation — clean code structure

- Regular investors: Don't touch it. At least not with real money.

Sources:

- TauricResearch/TradingAgents — Official repository

- GitHub Trending weekly ranking