Key Data

| Metric | Data |

|---|---|

| Power equipment investment growth | Expected to triple by 2030 |

| Data center share | Approximately 40% of total investment |

| Driver | AI data center construction boom |

What Does This Mean?

AI’s demand for power is shifting from “worth paying attention to” to “infrastructure-level reshaping.”

The 40% data center share means this: for every $10 invested in upgrading power systems, $4 goes to serving AI compute. This is not a marginal demand—it is the power industry’s new growth engine.

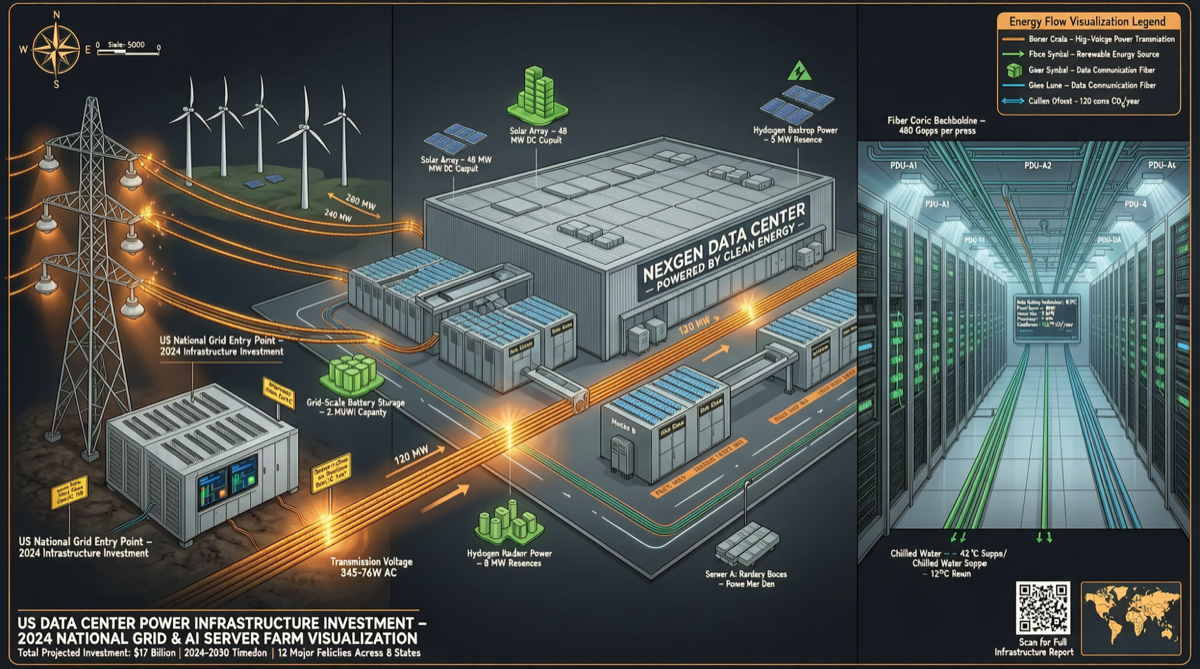

Supply Chain Impact

Upstream: Power Generation

- Nuclear power: Small Modular Reactor (SMR) projects are accelerating, tech companies directly investing in nuclear plants

- Natural gas: Baseload power during the transition period, demand continues to grow

- Renewable energy: Wind/solar paired with storage solutions becoming standard for data centers

Midstream: Transmission & Distribution

- Transformers: Surging demand extending delivery cycles from months to 1-2 years

- Grid upgrades: Aging grids need expansion to support new loads

- Energy storage: Lithium batteries and pumped hydro storage as peak-shaving measures

Downstream: Data Centers

- Site selection logic shifting: moving from proximity to users toward proximity to cheap power

- Liquid cooling becoming standard: air cooling can no longer meet heat dissipation needs of high-density GPU clusters

- Self-built power: tech giants directly participating in power generation and transmission facility construction

Investment Opportunities

| Track | Rationale | Risk |

|---|---|---|

| Power equipment manufacturers | Certain beneficiaries, full order books | Capacity bottlenecks, raw material price increases |

| Grid infrastructure | Policy + demand dual drivers | Long approval cycles |

| Nuclear SMR | Clear long-term growth logic | Technology maturity and regulatory risk |

| Energy storage | Peak-shaking essential demand | Fierce price competition |

| Data center REITs | Rent growth expectations | Long construction cycles, interest rate sensitivity |

Connection to the Chinese Market

China’s situation is similar but more complex:

- The East Data West Computing project is already optimizing the geography of power and compute

- Domestic GPUs (Huawei Ascend, etc.) energy efficiency directly affects power demand

- China’s power system has higher flexibility, but grid investment faces similar pressures

What This Means for Your Decisions

For AI startups: Compute costs are not just about GPU prices—they also include power costs. Site selection needs to consider electricity prices and power supply stability.

For investors: Power infrastructure follows the “pickaxe and water seller” logic in AI investment—regardless of which model company wins, power demand will grow.

For developers: Energy efficiency optimization for model inference (such as FlashQLA, FlashKDA, and other projects) is not just a technical issue—it directly impacts operational costs.

Timeline Assessment

Tripling by 2030 implies a compound annual growth rate of approximately 20%. This is not a sudden explosion, but a structural growth trend lasting 4-5 years. Power infrastructure construction cycles are much slower than AI model iteration—this is a slow-moving variable, but the direction is clear.