Core Numbers: One Quarter’s Capital Exceeds the Previous Decade

The Q1 2026 AI venture funding figures are in, and the conclusion is straightforward: this is no longer an “AI boom”—this is AI capitalization.

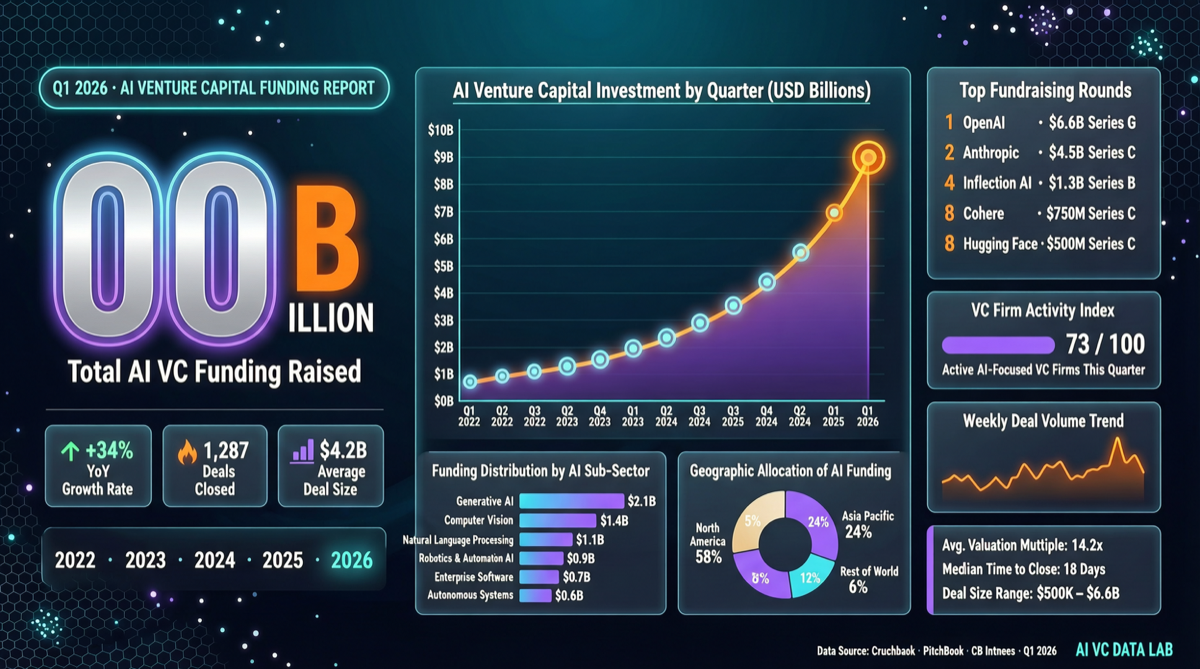

| Company | Funding Amount | Round | Lead Investors | Valuation/Use |

|---|---|---|---|---|

| OpenAI | $122B | Mega Round | SoftBank, Microsoft, Abu Dhabi | AGI Infrastructure |

| Anthropic | $30B | Series D | Amazon, Google | Claude Ecosystem Expansion |

| xAI | $20B | Series C | Multi-party consortium | Grok + X Integration |

| Waymo | $16B | Independent | Alphabet, External Investors | Robotaxi Expansion |

| Four Combined | $188B | — | — | 63% of Q1 Total |

Together, these four deals represent $188 billion—63% of total Q1 AI funding. The remaining 37% is spread across hundreds of startups. This is not a healthy distribution—it’s a classic “winner takes all” signal.

Where the Money Went: From Model Training to Ecosystem Building

Past funding rounds primarily targeted GPUs and training. In Q1 2026, the use of funds shifted noticeably:

- OpenAI’s $122B: Mostly allocated to global data center construction and AGI safety research, not just buying chips

- Anthropic’s $30B: Claude ecosystem expansion, including enterprise API, safety alignment research, and developer toolchains

- xAI’s $20B: Deep integration of Grok with the X platform—an attempt at a social+AI closed loop

- Waymo’s $16B: Moving from technology validation to commercial deployment, Robotaxi expansion across multiple cities

The trend is clear: leading companies are no longer raising funds just to “train bigger models”—they’re raising to “build bigger ecosystems.” This means the competitive dimension has shifted from model capability to platform effects.

Where Do Startups Fit In?

When four companies absorb 63% of available capital, remaining startups face stark choices:

- Go Vertical: Don’t build general models—build AI for specific use cases (healthcare, legal, finance)

- Open Source Differentiation: Follow the Hugging Face playbook—compete with community and transparency against closed ecosystems

- Get Acquired: Become part of a giant’s ecosystem rather than competing directly

- Expand Overseas: Seek differentiation in China, Southeast Asia, Middle East, and other markets

One notable signal: over 480 projects applied for the AI Discovery Awards 2026, competing for $100K in GPU cloud credits. This shows that startup enthusiasm hasn’t faded—but the bar for accessing capital has risen sharply.

Judgment and Recommendations

For Investors: The window for AI primary market investments is closing. The top-tier landscape is largely locked in. The next wave of opportunities lies in the application layer and vertical sectors.

For Entrepreneurs: If you’re building a foundation model, you need to articulate why investors should bet on you instead of OpenAI. If you’re building on top of large models, Q1 data shows that ecosystem niches are still rapidly fragmenting—vertical use cases still have significant whitespace.

For Professionals: Capital inflow means continued job demand expansion, but competition is intensifying too. Choosing between a platform company (OpenAI, Anthropic, xAI) and a vertical startup depends on your risk tolerance and career stage.